One year ago we announced the Sprout initiative at Shizen Capital.

Sprout is a GP-in-Training program for ambitious women in Japan who aspire to manage their own VC fund. The Sprout participant is first employed by Shizen Capital as Investment Director, during which she is exposed to all aspects of VC fund operations in a compressed timeframe. We attempt to convey to the best of our abilities the decades of experience we’ve gained from investing in startups (ideally minus our bad habits), and subsequently enable the Sprout participant to branch out as a GP with her own fund when she decides she is ready.

Our rationale in launching the Sprout program was driven by our observation of a pervasive lack of gender diversity in Japan’s venture capital sector. We believe that this pernicious issue negatively impacts VC fund returns, impedes female and other under-represented entrepreneurs, stifles the health of a region’s startup ecosystem, and deprives society as a whole of innovation.

In September, Mayumi Wakebe joined us as the inaugural Sprout candidate. Mayumi entered the program with a commendably open mind, i.e. she was graciously willing to serve as a pioneer (or test subject ?) for our pilot year. We believe perfection is the enemy of progress, so at Shizen Capital we prefer to launch experiments and then iterate as we go along. Mayumi joined us with exactly the right mindset compatible with this philosophy.

Not only has Mayumi survived; she has thrived ! Sure, we have been mentoring her along the way, but Mayumi has contributed disproportionately more to us in return.

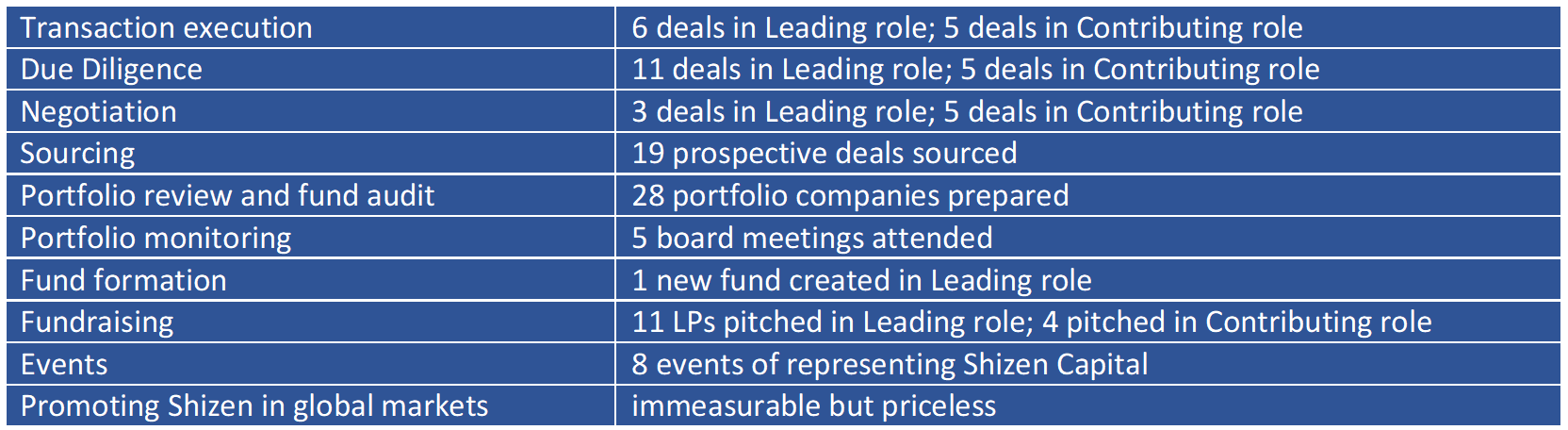

Let’s tally up Mayumi’s contributions to Shizen Capital in her first 9 months.

Some of you may be wondering why I am crowing about Mayumi’s contributions so publicly. My motivation is threefold:

- To boast. There’s nothing humble about this brag. I am truly proud.

- To publicly celebrate Mayumi. She’s very modest (in fact, she only reluctantly agreed to let me post this), and I believe that the world needs to hear how awesome she is.

- To inspire other VC funds in Japan to consider offering a GP fast-track to talented and ambitious women in VC. I know that many of our peers share our conviction on the value of gender diversity in VC. They are welcome to copy our playbook verbatim, or simply draw inspiration from it to tailor their own initiatives.

As an individual from another fund in Japan remarked, Mayumi has accomplished more in 9 months than they have been permitted to do over their career. Comments like this remind me that there remains much work to be done.